This post was part of a series about managing how you spend your investments, if you aim to live long, live within your means, and, perhaps, leave some for others. The main ideas have been updated and moved to an article on Retirement Income, on the Retired Now menu. If you wish, you can still read the original series, using the links below.

- Retail strategies, using all-in-one mutual funds. Simple solutions that work for some.

- Insurance strategies, using Social Security and maybe some annuities. Part of everyone's plan.

- Endowment strategies, adapted from foundations and universities. This post.

- Finance strategies, based on life-expectancy and future payments. Really good, simple methods.

- Smooth consumption, a comprehensive method that uses excellent, free software.

Setting Your Goals

When my father retired, he was fortunate to have inherited assets from my mother, who had died too young several years earlier, and from his own father. I remember my father saying his goal was to live on the interest and leave the principal for my three siblings and me. There was no way he could have known that the next decade would bring constant inflation and poor markets. A frugal spender who had no formal knowledge of finance or economics, he was happy, I suspect, to see the dollars in his account hold firm over the years, unaware that adjusted for inflation, they were worth much less than when his retirement began. I'm not complaining. He richly deserved every penny he spent, and then some.

Looking back on my father's experience and thinking ahead to my own retirement, I would reframe his twin goals of living on interest and preserving principal. Instead, for any retiree, I see the objectives as a triplet:

Looking back on my father's experience and thinking ahead to my own retirement, I would reframe his twin goals of living on interest and preserving principal. Instead, for any retiree, I see the objectives as a triplet:

- Covering expenses. As noted earlier in this series, insured income from Social Security, possibly supplemented by a lifetime, inflation-adjusted annuity, may partially achieve this goal. The rest would come from managed investments.

- Holding emergency reserves. Unless one's retirement accounts are very large, some portion should be managed separately for unplanned expenses such as uninsured medical costs, accidental damage to property, or dependents' unforeseen needs.

- Leaving a bequest. For those lucky enough to have assets exceeding their own needs for normal expenses and emergency reserves, the remaining funds may be managed as future gifts, donations, or inheritances.

Historical Analysis

Previously, I described a set of historical data on U.S. stock and bond markets since 1924, with which I studied the experience of hypothetical investors, all of whom retired at age 65 and lived to 95. The analysis had 62 cohorts, each starting in January of a year between 1924 and 1985, and ending 30 years later in December of a year between 1974 and 2015. For these cohorts, I considered three methods of managing retirement funds.

- Flat Percentage. Annually, a fixed percentage is withdrawn from a retirement account, while the remainder is left to grow over time. Variants of this method turn out to work best for managing emergency reserves. The method is similar to how universities and foundations typically manage their endowments.

- Required Minimum Distributions (RMD) . As dictated by the Internal Revenue Service, retirees at 70.5 years and older must withdraw a portion of their traditional IRA, 401(k), 403(b) or 457 accounts annually and pay taxes on the amount withdrawn. Each year, the mandatory portion increases, because the tax-collectors want their due. Consequently, the RMD method works poorly for emergency reserves and bequests. By design, it depletes the accounts of those who live long lives. It won't preserve a surplus for unexpected needs or posterity. Furthermore, if reserves or gifts are held in Roth or taxable accounts, as may be advantageous, then withdrawals are not obligatory, and the RMD method is irrelevant.

- Inflated 4%. This method withdraws 4% of an account's initial value at the start of retirement, then increases the withdrawn dollars each year by the same percentage as the previous year's inflation in consumer prices, or, less commonly, decreases it by the amount of deflation. It's really a variant of the flat-percentage method, but one that risks depletion of the account if inflation runs high for many years. For this reason, it's a non-starter for all except very short retirements.*

Emergency Reserves: Typical Outcomes

I first looked at a portfolio with 35% in U.S. stocks, 50% in 10-year U.S. treasury bonds, and 15% in 2-year U.S. treasury notes. Allocating 35% to stocks was a compromise between capturing the long-term, inflation-beating power of stocks and earning the shorter-term, stable return of bonds. In my previously reported study of inflation, a 35% allocation was a good choice for funds likely to be spent five to six years in the future, which seems reasonable as a planning target for retirement reserves. Coincidentally, the retirement income funds offered by most investment firms allocate 30% or 40% to stocks. Perhaps they should be renamed "retirement reserve funds" and relegated to the emergency-reserve portion of one's portfolio.

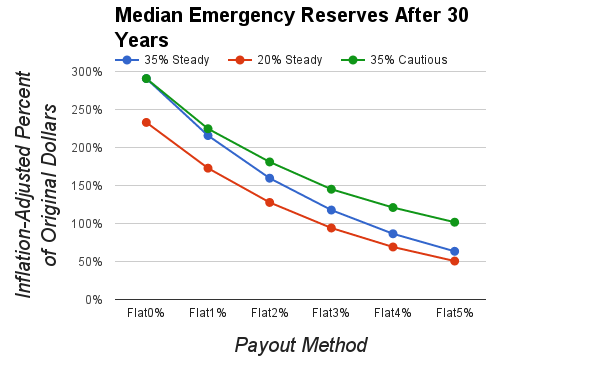

The chart below summarizes the simulated outcomes at the end of a 30-year retirement, for withdrawal rates ranging from 0% to 5% annually. The blue line labeled "35% Steady" shows the amount remaining after 30 years, for the middle cohort, using the 35% allocation to stocks and steady withdrawals every year. Half the cohorts did better than the blue line; half did worse. For example, at Flat0%, where nothing was ever withdrawn, the middle cohort's reserve fund had nearly tripled in buying power after 30 years. Even for Flat3%, where each year the retiree spent 3% of the reserves, the middle cohort kept 100% of its original buying power. Nice!

The chart below summarizes the simulated outcomes at the end of a 30-year retirement, for withdrawal rates ranging from 0% to 5% annually. The blue line labeled "35% Steady" shows the amount remaining after 30 years, for the middle cohort, using the 35% allocation to stocks and steady withdrawals every year. Half the cohorts did better than the blue line; half did worse. For example, at Flat0%, where nothing was ever withdrawn, the middle cohort's reserve fund had nearly tripled in buying power after 30 years. Even for Flat3%, where each year the retiree spent 3% of the reserves, the middle cohort kept 100% of its original buying power. Nice!

For comparison, I ran simulations for two additional portfolios as depicted in the chart. One, called "20% Steady" and shown by the red line, had a more conservative allocation: 20% stocks, 60% 10-year bonds, and 20% 2-year bonds. Because of the lower allocation to stocks, the returns tended to be a bit lower. Even so, after 30 years of withdrawing 3% annually, the middle cohort had virtually all its original buying power.

The final portfolio, shown by the green line labeled "35% Cautious," was the best of all. It had exactly the same allocations to stocks and bonds as the 35% Steady portfolio, but the method of withdrawal was modified. If, in the previous year, the portfolio had fallen in value, then no withdrawal was taken. However, if the previous year had positive returns, then 1% to 5% was withdrawn, as depicted in the chart. This method simplifies more elaborate strategies that many endowments use to moderate their withdrawals depending on the results of prior years. It's also what your instincts might guide you to do. After a down year, you might find yourself taking no discretionary withdrawals, while waiting for your funds to recover. That's exactly how the "35% Cautious" simulation worked, with favorable results.

Because of normal, non-discretionary expenses, you might not be able to delay withdrawals from the rest of your retirement assets after a bad year. But non-emergency withdrawals from your reserve fund are truly discretionary. They allow you to redirect surplus funds to a vacation, to charitable donations, or to your fund for future bequests. When markets are falling, you can skip them.

The final portfolio, shown by the green line labeled "35% Cautious," was the best of all. It had exactly the same allocations to stocks and bonds as the 35% Steady portfolio, but the method of withdrawal was modified. If, in the previous year, the portfolio had fallen in value, then no withdrawal was taken. However, if the previous year had positive returns, then 1% to 5% was withdrawn, as depicted in the chart. This method simplifies more elaborate strategies that many endowments use to moderate their withdrawals depending on the results of prior years. It's also what your instincts might guide you to do. After a down year, you might find yourself taking no discretionary withdrawals, while waiting for your funds to recover. That's exactly how the "35% Cautious" simulation worked, with favorable results.

Because of normal, non-discretionary expenses, you might not be able to delay withdrawals from the rest of your retirement assets after a bad year. But non-emergency withdrawals from your reserve fund are truly discretionary. They allow you to redirect surplus funds to a vacation, to charitable donations, or to your fund for future bequests. When markets are falling, you can skip them.

Emergency Reserves: Worst Cases

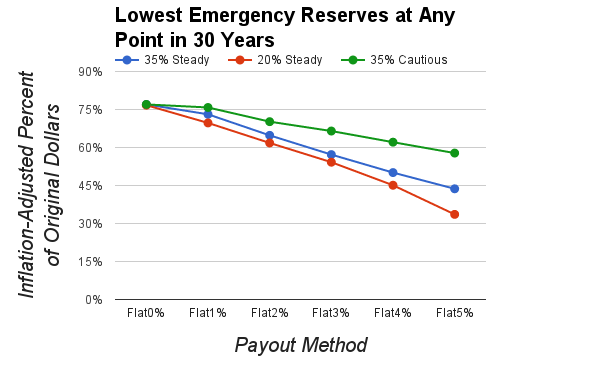

If an emergency requires you to spend your reserves, it matters little what they might hypothetically earn after 30 years. You need them now. What matters, from this perspective, is the least amount you can expect to be available at any point during your retirement, not the cumulative total at the end. Accordingly, my simulations calculated the low-point for each payout method, over all 62 portfolios and all 30-year periods. For a given method, that's the lowest of 62 times 30 or 1860 outcomes. It's truly a worst-case metric, one that's lower than the other 99.95% of the method's historical results. The next chart shows this metric for each simulation.

As one example, for the 35% Steady portfolio and 2% withdrawals every year, the most dismal cohort sank to about 65% of its original buying power at one point during its 30-years of retirement. One might think that a more conservative portfolio, with less allocated to stocks, would be less volatile and thus suffer less depletion. Not so! Comparing the red and blue lines in the chart, it's clear that the more conservative 20% portfolio actually sank to lower lows than the 35% portfolio. How could this be? The reason, in brief, is that during periods of high inflation, the interest rate on bonds has often been less than the current inflation rate. A heavier allocation to bonds, if it lasts long enough during such times, will reduce inflation-adjusted returns.

The best strategy for limiting losses, across all the simulations, turned out to be the same as the one that was best for promoting gains. It was the 35% Cautious method.

The best strategy for limiting losses, across all the simulations, turned out to be the same as the one that was best for promoting gains. It was the 35% Cautious method.

Summing Up

This analysis has several implications for retirees.

- The retirement income funds offered by many investment firms, with about 30% to 40% allocated to stocks, may be a good match for funds you set aside as emergency reserves during retirement. This does not mean you should put all your assets in such funds, just the portion necessary for emergencies.

- If the future is like the past, then in most years you may be able to spend a modest percentage of your reserve fund, without losing any of its purchasing power, long-term. About 1% to 3% may be prudent.

- Your instinctive tendency to scale back spending after a bad year may be wise, at least for discretionary withdrawals from your reserve fund.

* Endowments sometimes use cost-increases or inflation as part of their strategy for determining withdrawals. However, to curtail the risk of depletion, they add "collars" that prevent the withdrawn amount from growing faster than a certain rate compared to previous years. Should you be inclined to try such methods, you can find a very simple, very effective version in the post on finance strategies, or more elaborate versions here for Yale University and here for three other institutions.

Although a mixture of bonds, stocks, and guaranteed benefits may be safer than investing exclusively in one class of assets, diversification cannot guarantee a positive return. Losses are always possible with any investment strategy. Nothing here is intended as an endorsement, offer, or solicitation for any particular investment, security, or type of insurance.

RSS Feed

RSS Feed