NOTE: For better, more current information about rotated portfolios, go to: likelyso.com/money.

My posts since June have used historical data to introduce rotation as way to manage a diversified portfolio of stocks and bonds. Today's post launches an ongoing series of updates that will review how rotation works in real time, month by month, on a sample set of portfolios. Initially, the updates will be posted here. In time, they will move to a subscription newletter.

Sample Portfolios

Some of the portfolios use low-fee Exchange-Traded Funds (ETFs) available in any brokerage account; others use low-fee mutual funds similar to those typically available in 401(k) and 403(b) retirement plans. The funds and ETFs track well-defined indexes or, in exceptional cases, use quantitative methods that limit the discretion of the fund's manager. Some of the portfolios use a short three-month window to decide which ETFs or funds to hold; others use a longer 12-month window.

The portfolios were constructed from simulations that used at least 25 years of monthly historical data. Going forward, actual performance will be updated once a month. A strict rule for all the portfolios is that any change in a portfolio's composition is held at least until the next monthly update.

The sample portfolios are organized in four groups, corresponding to four types of investment goals or risk tolerances. Today's updates provide one example in each group. Other examples will be added in coming weeks.

My posts since June have used historical data to introduce rotation as way to manage a diversified portfolio of stocks and bonds. Today's post launches an ongoing series of updates that will review how rotation works in real time, month by month, on a sample set of portfolios. Initially, the updates will be posted here. In time, they will move to a subscription newletter.

Sample Portfolios

Some of the portfolios use low-fee Exchange-Traded Funds (ETFs) available in any brokerage account; others use low-fee mutual funds similar to those typically available in 401(k) and 403(b) retirement plans. The funds and ETFs track well-defined indexes or, in exceptional cases, use quantitative methods that limit the discretion of the fund's manager. Some of the portfolios use a short three-month window to decide which ETFs or funds to hold; others use a longer 12-month window.

The portfolios were constructed from simulations that used at least 25 years of monthly historical data. Going forward, actual performance will be updated once a month. A strict rule for all the portfolios is that any change in a portfolio's composition is held at least until the next monthly update.

The sample portfolios are organized in four groups, corresponding to four types of investment goals or risk tolerances. Today's updates provide one example in each group. Other examples will be added in coming weeks.

All-Max Portfolios

The dominant goal of an all-max portfolio is to maximize total return in the long run. It aims to hold equities rather than bonds, except when bonds are demonstrably performing better than equities. The guiding principle is to rotate out of stocks and into bonds when the total return of stocks, relative to that of bonds, has weakened, or vice versa. The portfolio may be 100% in stocks or 100% in bonds. However, if the portfolio has more than one equity ETF or fund, such as one for domestic U.S. companies and another for international ones, then it may sometimes hold a mixture of stocks and bonds. That may happen, for example, if U.S. equities are stronger than bonds, but international equities are not.

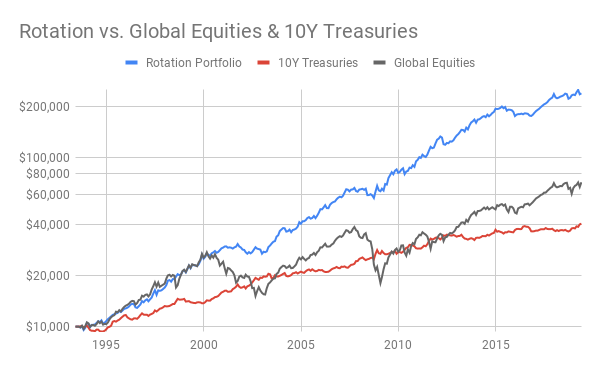

Today's example for this group, shown in the chart above, is All-Max Global Markets 100-to-0 ETFs. It is contructed from four ETFs that track broad indexes of domestic and international stocks and U.S. Treasury bonds. At a given time, each ETF is 0%, approximately 25%, or approximately 50% of the portfolio, with a 5% variance that triggers rebalancing. The ETFs and their current allocations are:

A forthcoming post will provide details on a 25-year simulation of this portfolio. In markets without a steady trend, including most of the past year, the portfolio's three-month window for evaluating ETF performance may generate choppy results. However, over the past decade or longer, it has outperformed benchmarks such as Vanguard's LifeStrategy Growth Fund or the composite of global equities, as the chart demonstrates.

The dominant goal of an all-max portfolio is to maximize total return in the long run. It aims to hold equities rather than bonds, except when bonds are demonstrably performing better than equities. The guiding principle is to rotate out of stocks and into bonds when the total return of stocks, relative to that of bonds, has weakened, or vice versa. The portfolio may be 100% in stocks or 100% in bonds. However, if the portfolio has more than one equity ETF or fund, such as one for domestic U.S. companies and another for international ones, then it may sometimes hold a mixture of stocks and bonds. That may happen, for example, if U.S. equities are stronger than bonds, but international equities are not.

Today's example for this group, shown in the chart above, is All-Max Global Markets 100-to-0 ETFs. It is contructed from four ETFs that track broad indexes of domestic and international stocks and U.S. Treasury bonds. At a given time, each ETF is 0%, approximately 25%, or approximately 50% of the portfolio, with a 5% variance that triggers rebalancing. The ETFs and their current allocations are:

- Vanguard Total Stock Market ETF (VTI). Now at 0%, its target level had been 25% in July.

- Vanguard FTSE Developed Markets ETF (VEA): Its current level is 0%, as it has been since June 1.

- Vanguard Long-Term Treasury ETF (VGLT): Its target level is 50% now, as it was in July.

- Vanguard Intermediate-Term Bond Index ETF (BIV): Now at 50%, it received the proceeds from selling VTI on August 1.

A forthcoming post will provide details on a 25-year simulation of this portfolio. In markets without a steady trend, including most of the past year, the portfolio's three-month window for evaluating ETF performance may generate choppy results. However, over the past decade or longer, it has outperformed benchmarks such as Vanguard's LifeStrategy Growth Fund or the composite of global equities, as the chart demonstrates.

Mostly-Max Portfolios

In this group, the blended goals are, primarily, to maximize total returns and, secondarily, to minimize drawdowns. For partial protection against sudden drawdowns, a mostly-max portfolio always holds a minority of its assests in a bond fund or ETF. It aims to hold a substantial majority in equities when they are strong relative to bonds, rotating to 100% in bonds only when stocks have weakened.

For this group, today's example is Mostly-Max Low Volatility 80-to-0 ETFs. See my recent post for a 25-year simulation of this portfolio. It is composed of the following ETFs, whose target levels remain unchanged from last month:

This portfolio compares ETFs on a 12-month window and therefore tends to hold a postion for many months. In a forthcoming post, a similar portfolio using mutual funds will highlight the performance of Vanguard's excellent Global Minimum Volatility Fund (VMVFX).

In this group, the blended goals are, primarily, to maximize total returns and, secondarily, to minimize drawdowns. For partial protection against sudden drawdowns, a mostly-max portfolio always holds a minority of its assests in a bond fund or ETF. It aims to hold a substantial majority in equities when they are strong relative to bonds, rotating to 100% in bonds only when stocks have weakened.

For this group, today's example is Mostly-Max Low Volatility 80-to-0 ETFs. See my recent post for a 25-year simulation of this portfolio. It is composed of the following ETFs, whose target levels remain unchanged from last month:

- iShares Edge MSCI Minimum Volatility USA (USMV). Currently 60%.

- iShares Edge MSCI Minimum Volatility EAFE (EFAV). Currently 0%.

- Vanguard Total World Bond ETF (BNDW). Currently 20%. It may rotate to 0% or to as much as 80%. BNDW holds equal portions of Vanguard's broad indexes for U.S. and international bonds.

- Vanguard Long-Term Bond ETF (BLV). Always 20%, as a hedge against sudden drawdowns.

This portfolio compares ETFs on a 12-month window and therefore tends to hold a postion for many months. In a forthcoming post, a similar portfolio using mutual funds will highlight the performance of Vanguard's excellent Global Minimum Volatility Fund (VMVFX).

Mostly-Min Portfolios

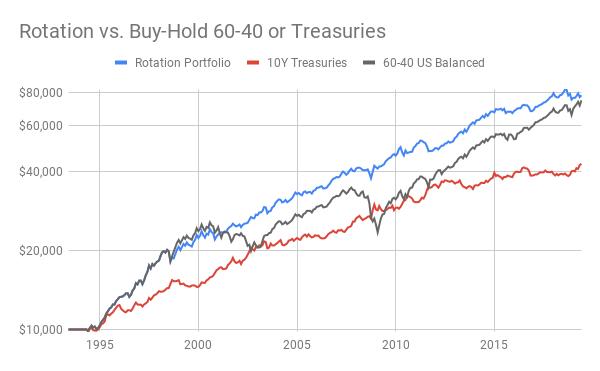

The blended goals of this group are, with high priority, to minimize drawdowns and, with less weight, to boost total returns. Today's example for this group is Mostly-Min US Balanced 60-or-0 Fund. As the chart above illustrates, the total return of this portfolio over the past 25 years has modestly exceeded a standard 60-40 mix of U.S. stocks and bonds. In doing so, the mostly-min portfolio avoided major drawdowns and matched the low volatility of 10-year Treasuries. The very simple strategy of this portfolios is always to invest entirely in one of three indexed mutual funds:

Normally, the portfolio rotates between the 60-40 balanced fund and the intermediate bond fund. However, to limit flip-flops and to honor the restrictions on frequent trading that investment firms and retirement plans typically impose, the portfolio will, on rare occasions, hold all its assets in the short-term bond fund. A detailed post later this month will explain the mechanics and long-term performance of this portfolio, including details about when and why to hold the short-term bond fund.

The blended goals of this group are, with high priority, to minimize drawdowns and, with less weight, to boost total returns. Today's example for this group is Mostly-Min US Balanced 60-or-0 Fund. As the chart above illustrates, the total return of this portfolio over the past 25 years has modestly exceeded a standard 60-40 mix of U.S. stocks and bonds. In doing so, the mostly-min portfolio avoided major drawdowns and matched the low volatility of 10-year Treasuries. The very simple strategy of this portfolios is always to invest entirely in one of three indexed mutual funds:

- Vanguard Balanced Index Fund (VBIAX), which targets 60% in U.S. equities and 40% in U.S. bonds.

- Vanguard Intermediate-Term Bond Index (VBILX), which invests 100% in diversified U.S. bonds. This fund has held 100% of the portfolio's assets since June 1.

- Vanguard Short-Term Bond Index (VBIRX), which the portfolio occasionally uses for temporary holdings.

Normally, the portfolio rotates between the 60-40 balanced fund and the intermediate bond fund. However, to limit flip-flops and to honor the restrictions on frequent trading that investment firms and retirement plans typically impose, the portfolio will, on rare occasions, hold all its assets in the short-term bond fund. A detailed post later this month will explain the mechanics and long-term performance of this portfolio, including details about when and why to hold the short-term bond fund.

All-Min Portfolios

Here the overarching goal is to minimize drawdowns in a portfolio that never has more than a minority exposure to equities. The example today is All-Min Global Income 30-or-0 Fund. It has a simple strategy of investing all its assets in one of three indexed mutual funds:

Normally, the portfolio holds either the 30-70 income fund or the intermediate Treasury fund for many consecutive months. However, to limit churn and honor restrictions on frequent trading, it may sometimes hold the short-term bond fund for a month or two. As will be documented in a forthcoming post, the rotation strategy of this all-min portfolio has, historically, achieved higher total returns with smaller drawdowns than investing exclusively and continously in either of its two main alternatives, the 30-70 fund or intermediate Treasuries.

Here the overarching goal is to minimize drawdowns in a portfolio that never has more than a minority exposure to equities. The example today is All-Min Global Income 30-or-0 Fund. It has a simple strategy of investing all its assets in one of three indexed mutual funds:

- Vanguard Target Retirement Income Fund (VTINX), which targets 30% in global equities and 70% in worldwide bonds, including some that are indexed to U.S. inflation.

- Vanguard Intermediate-Term Treasury Index (VSIGX). All the portfolio's assets have been invested here since January, and remain so this month.

- Vanguard Short-Term Bond Index (VBIRX).

Normally, the portfolio holds either the 30-70 income fund or the intermediate Treasury fund for many consecutive months. However, to limit churn and honor restrictions on frequent trading, it may sometimes hold the short-term bond fund for a month or two. As will be documented in a forthcoming post, the rotation strategy of this all-min portfolio has, historically, achieved higher total returns with smaller drawdowns than investing exclusively and continously in either of its two main alternatives, the 30-70 fund or intermediate Treasuries.

Disclosures

These portfolios are presented for information only, not as investment advice. They are based on simulations that may not capture or reproduce every aspect of actual investing. Historical results are no guarantee of future performance. All investments are subject to risks. You may lose money, and your assets may be vulnerable to inflation. You are responsible for your own investment decisions.

Able to Pay LLC does not own, sell, or manage any of these portfolios. Alex Wilkinson may own similar portfolios in personal accounts.

These portfolios are presented for information only, not as investment advice. They are based on simulations that may not capture or reproduce every aspect of actual investing. Historical results are no guarantee of future performance. All investments are subject to risks. You may lose money, and your assets may be vulnerable to inflation. You are responsible for your own investment decisions.

Able to Pay LLC does not own, sell, or manage any of these portfolios. Alex Wilkinson may own similar portfolios in personal accounts.

RSS Feed

RSS Feed